Reliance's Smart Financial Engineering for Jio's Debt

An astute understanding of financial instruments and the acumen to use them optimally are what worked in Reliance Industries' favor.

We have a very clear roadmap to becoming a zero-net-debt company in the next 18 months, that is, by 31st March 2021.

- Mukesh Ambani at Reliance Industries’ 42nd AGM

As a follow-up to an earlier post on Side Notes - Why did Reliance Jio need money when it already had enough?, this post explores the financial engineering that went behind raising that money.

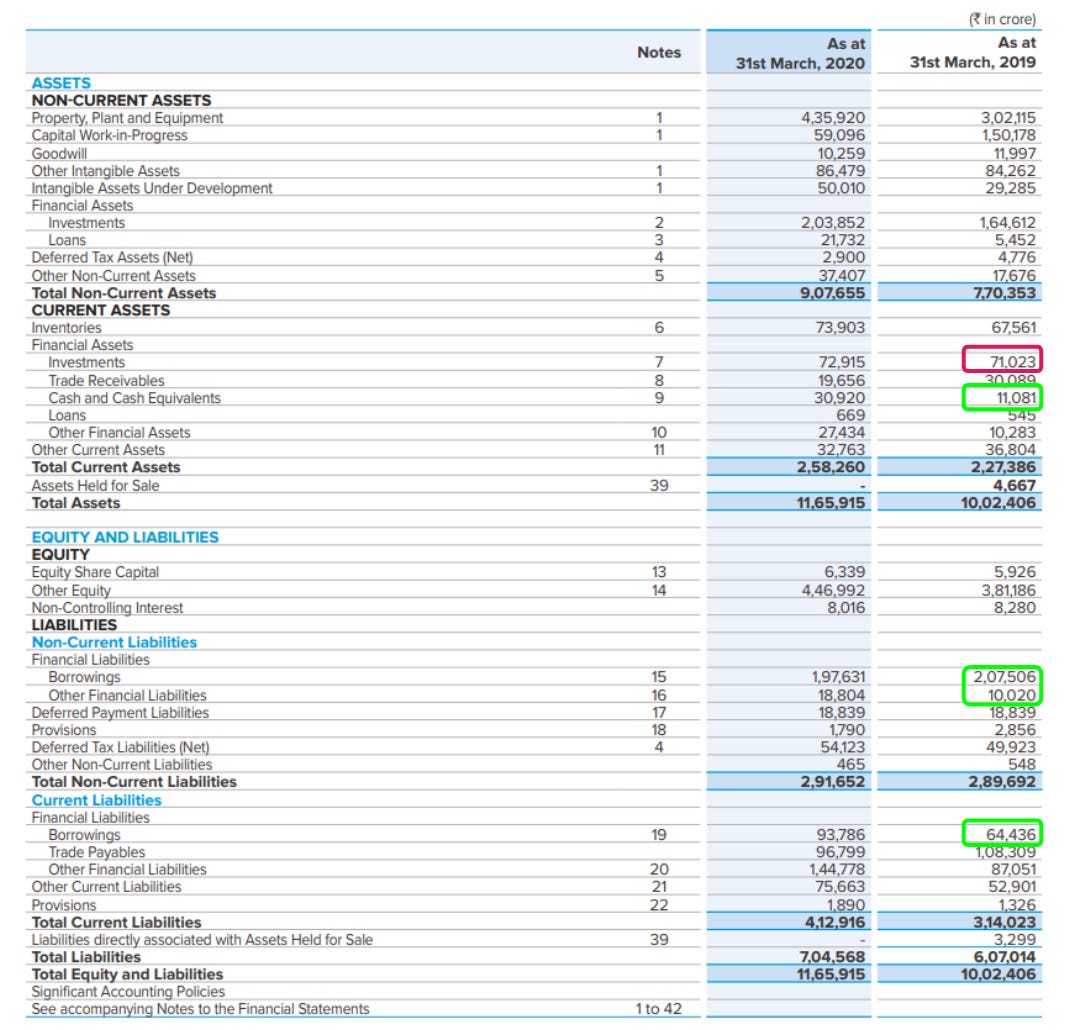

When Mr. Ambani made that statement in 2019, Reliance Industries had a total debt of over ₹2.8 lakh crore, and a net debt of over ₹2.1 lakh crore. First of all, yes, it is “lakh crore”. Reliance operated and still operates at that scale.

But what is the difference between total debt and net debt?

Total debt is the sum of a company’s long and short-term borrowings. Net debt is total debt minus the company’s cash and cash equivalents. It shows the amount of debt that would remain on a company’s balance sheet if it were to utilize all its available liquidity.

Mr. Ambani said that Reliance was going to become zero-net-debt, and not zero-debt. But that is okay, too. Think of it this way: if you have 100 in borrowings but 200 in cash, you are essentially debt-free. You might still have kept the borrowings because perhaps investing the cash is yielding better returns than the interest you are paying on the borrowed amount.

The roadmap to becoming net debt-free had two parts to it.

Set up a JV with BP and transfer the existing fuel retail network and the aviation fuel business to the JV. BP would pay 7000 crores to Reliance Industries for its 49% stake in the JV.

Sell 20% stake in the Oil-to-Chemicals business to Saudi Aramco for an enterprise valuation of $75 billion.

The twin deals with BP and Saudi Aramco were going to raise over ₹1.2 lakh crore. As of March 2019, Reliance had a net debt of over ₹2.1 lakh crore. That number is based on the conventional formula of Total Debt minus Cash and Equivalents.

However, Reliance calculated it a little differently. Not just cash and equivalents, it also subtracted all its current investments from total debt. Although analysts did not agree, that approach brought the net debt down to about 1.6 lakh crore. So yes, accounting for current investments, zero-net-debt was a real possibility.

However, the Saudi Aramco deal hit a roadblock. After over two years, in late 2021, the negotiations were called off, and Aramco never invested in Reliance’s O2C business.

Nonetheless, Reliance achieved zero-net-debt status about nine months earlier in June 2020. It managed to do so in two ways, neither of which was part of the initial plan.

It raised ₹1.15 lakh crore from global tech investors for Jio Platforms (more investments came after the zero-net-debt status)

It raised over ₹53,000 crore through a rights issue in May 2020.

As far as the rights issue was concerned, of course, there was no tax incidence to it. It was just fresh equity being raised.

The tricky part was the funds raised for Jio Platforms. See, Jio Platforms was spun off as a subsidiary of Reliance Industries. If Jio Platforms issued fresh equity to the global tech investors, that money would belong to Jio Platforms. For Reliance to use those funds, it would have to draw dividends. But dividends cannot be given selectively to just one or a few shareholders. All shareholders are entitled to dividends. So the tech investors would also get dividends. That would make no sense - they had just invested the funds.

RIL could have also taken a loan from Jio Platforms to get those funds. But taking a loan to pay off the loan would defeat the purpose. Reliance would still have that debt on its books.

Another option was for Reliance to sell its stake in Jio Platforms to the tech investors. Jio Platforms was only recently incorporated in November 2019. The global investors had started investing in early 2020. Therefore, if Reliance had sold its stake to those investors, it would have incurred short-term capital gains tax, which would have been upwards of ₹20,000 crores.

Reliance Industries found a way out of it. Here is what it did to get the funds and save on taxes.

There were multiple entities involved, but we will keep it simple to understand the flow of money.

First, Reliance Industries set up a subsidiary, Jio Platforms, in November 2019. The telecom business and the digital services businesses were all transferred to Jio Platforms. To begin with, Jio Platforms had an equity of ₹65,000 crores, all of which was owned by RIL. Of that, about ₹4,500 crore was common equity, the rest was Optionally Convertible Preference Shares (OCPS).

OCPS are preference shares that can be converted into common shares if the preference shareholder wants to do so. There is no obligation to convert, though.

While offering free plans for the first few years upon its launch and for setting up the nationwide network, Jio had taken on massive debt. It amounted to ₹1.08 lakh crore. This debt was also on the books of Jio Platforms.

Jio Platforms had a fat balance sheet with ₹65,000 crore in equity and ₹1.08 lakh crore in debt. That is a debt-to-equity ratio of 1.7 times.

Reliance wanted external investors, specifically, the global tech investors, to invest in Jio Platforms. However, with so much debt on its books, it was not a very lucrative investment.

So Jio Platforms transferred the debt to Reliance Industries. How did Jio Platforms pay for the transfer? By issuing equity. More specifically, by issuing OCPS.

Reliance Industries took over debt worth ₹1.08 lakh crore and received an OCPS of the same amount in Jio Platforms. The total equity was approximately ₹1.73 lakh crore, while the OCPS equity was around ₹1.69 lakh crore.

Now, Jio Platforms was debt-free. The global tech investors were lining up to invest. Observers assumed that RIL would sell its OCPS to those investors. But Jio Platforms issued fresh common equity shares to raise over ₹1.52 lakh crore from 13 marquee investors against a 33% stake.

Jio Platforms was flush with cash. RIL, instead of converting its OCPS into common equity, redeemed ₹1.29 lakh crore worth of OCPS, or rather encashed them. The cash that external investors had infused in Jio Platforms was used to pay for RIL’s OCPS.

There were two spots where Reliance might have had to pay taxes, but did not.

Had it sold its own stake in Jio Platforms to external investors, it would have incurred taxes. However, those investors got fresh equity. There was no stake sale. Hence, there was no tax incidence.

The OCPSs were redeemed at the price at which Reliance had acquired them, and not at a higher price. So, Reliance had no capital gains and hence had no taxes to pay.

The amounts of ₹1.29 lakh crore that RIL redeemed from Jio and the ₹53,000 crores raised from the rights issue more than covered the ₹1.6 lakh net debt Reliance had. Effectively, with more cash than debt, Reliance achieved a zero-net-debt status in June 2020.

That situation was short-lived, as Reliance went on to take on more debt for expansion across its business verticals, including retail, oil-to-chemicals, and Jio.

What remains interesting is how Reliance managed to save so much in taxes while being on the right side of the law.

You may also check out Side Notes on Spotify and Apple.

This Newsletter is written by Vineet Rajani.

Do read “Why do stock markets have circuit breakers?” in our newsletter, Tell Me Why by Zerodha Varsity.

For any feedback or topic suggestions, write to us at varsity@zerodha.com

Great article.. Will come back again for 3rd look...