How can dividends exceed earnings?

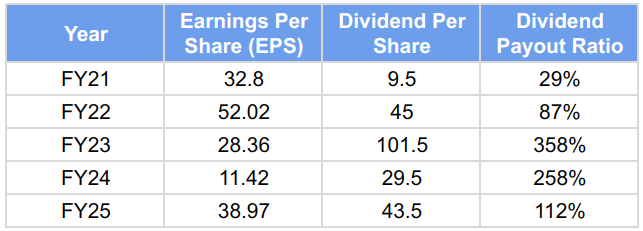

Vedanta’s 3-year average dividend payout ratio is 243%, which is unusual for any company

If profits are a cake, dividends are a pie from that cake.

But can the pie be bigger than the cake? If dividends are paid out of profits, how can the dividends be larger than the profits?

There might be several companies doing that, but I came across one such company - Vedanta Ltd.

First, the basics. When a company makes profits, it distributes some or all of those profits to its shareholders. The amount of profit distributed to shareholders is called a dividend. The amount it did not distribute is called retained earnings.

You can also listen to this newsletter on Apple Podcasts or Spotify.

In July 2022, Vedanta paid an interim dividend of 19.5 per share. Naturally, if the dividend was paid in July, it was for the quarterly result of the April-June quarter of that year. In that particular quarter, Vedanta’s net consolidated profit was 11.92 per share. The dividend per share was much higher than the EPS.

In fact, in FY23, Vedanta paid total dividends of 101.5 per share when its earnings per share were 28.5.

Now, the question is how Vedanta could pay more dividends than its earnings and how it does this.

Like I explained earlier, the part of profits not distributed as dividends is called retained earnings. It remains with the company. The company can use the retained earnings to pay off some loans, invest in new business opportunities, or just hold them as reserve funds.

If the retained earnings are held as a reserve, they can be used for any new opportunity that arises in the future. These reserves are also useful if the business slows down. If the company suffers losses in a particular period, it can use these reserves to continue its operations.

While companies usually don’t use reserves to pay dividends, there is nothing that prevents them from doing so.

In fact, some companies may even take out loans and pay dividends. The issue is that such a move adds debt while reducing equity. When dividends are paid, reserves go down, so equity also goes down. At the same time, when the loan goes up, the debt also goes up.

So the debt-equity ratio skews further.

In fact, Vedanta did both in FY23. One, it used up nearly half of the reserves it had created from the retained earnings of the past years. And two, it also took some short-term and long-term loans to pay the hefty dividends that were almost 3.5 times the size of its earnings that year.

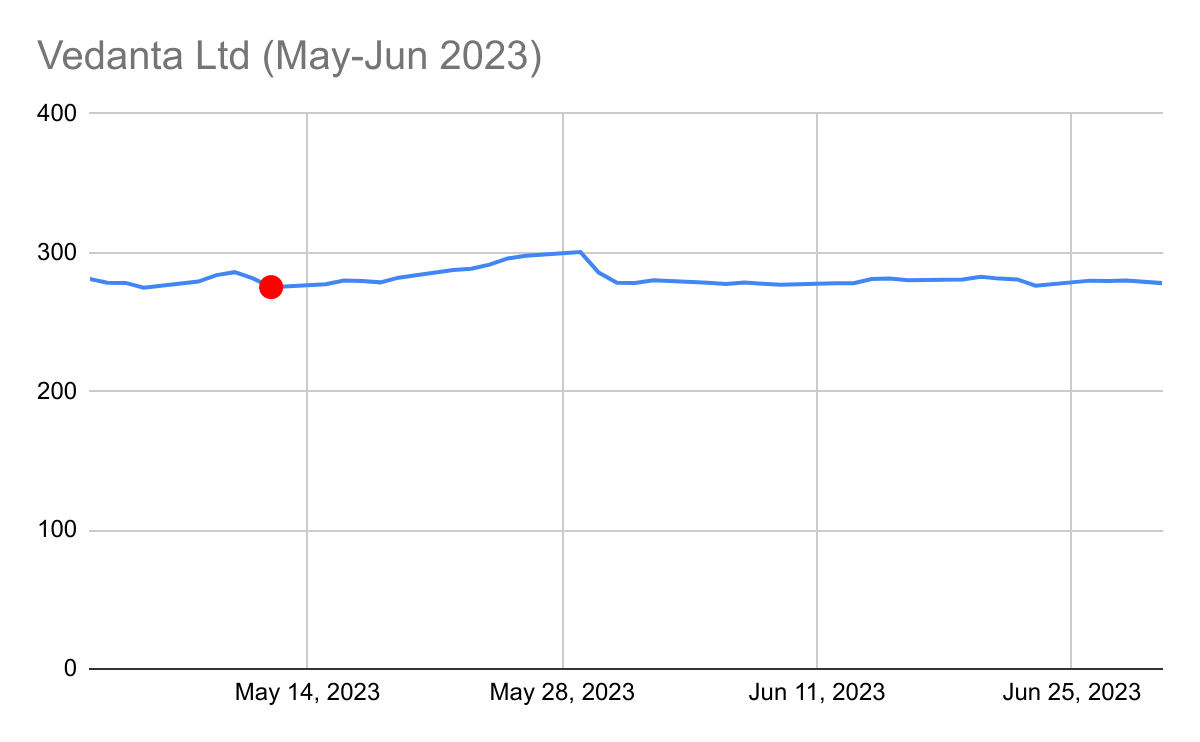

And yes, its debt-to-equity ratio also worsened. Its net debt was 46% of the equity in the previous year, FY22. After paying dividends, net debt climbed to 116% of equity in FY23.

That is a massive jump in debt with no comparative growth in assets or new business opportunities. Perhaps the market was as excited about the high dividend payout as it was worried about the rising leverage. Maybe that’s why the stock price remained largely flat in the weeks after the dividend announcement.

Why would a company pay such high dividends that exceed earnings? Usually, when a company has built up a huge reserve pile and the management realizes that it really won’t need so much to invest in the future, it decides to distribute some of it among the shareholders.

It can do so in two ways:

One is that they can do share buybacks. I won’t get into buybacks now, but I promise to write a separate post on them.

The other option is to declare an extraordinary dividend. The term extraordinary is used to suggest that this is a one-time payout, and the shareholders must not expect such a payout anytime soon in the coming years.

However, Vedanta did not call any of the interim dividend payouts that year as extraordinary dividends.

Does that mean it is going to keep paying such high dividends every year? Unlikely.

But in the very next year, that is in FY24, it paid a dividend of 29.5 per share, when its earnings per share were just 11.4. If you noticed, in FY24, both earnings and dividends declined but dividend payouts were again much larger than the earnings.

Maybe Vedanta’s management does not feel the need to hold so much reserves on its books. Maybe it is part of the restructuring process that the organization is going through. There have been talks of splitting the business into 6 independent businesses. Maybe they want to distribute cash to all shareholders equally before splitting and making it six different businesses of different sizes.

On a side note, while FY24 earnings were cut in half, Vedanta’s ROE did not fall as much. Because it paid huge dividends, its equity base had fallen. The numerator had become smaller. That's why, despite a 50% decline in earnings, Vedanta’s ROE only slid from 22% in FY23 to 16.5% in FY24.

It is usually a matter of concern when dividends exceed profits. However, the devil, or value, is in the details. Look closely and you will make a more informed decision🙂.

This newsletter is written by Vineet Rajani.

Do read Why did meme stocks suddenly become popular? in our newsletter, ‘Tell Me Why’ by Zerodha Varsity.

For any feedback or topic suggestions, write to us at varsity@zerodha.com

High payouts appear timed before split, favoring insiders with significant ownership. Hah! Insiders want to grab as much money as they can in whatever way they can 🙃 - before the firm splits into 5 entities with a weaker cashflow-reserve which means less value for the retail investors in the long term.

Eat! Eat! Eat! Before others join the party! 😁

As per 2(22)b of Income tax act, this amounts to distribution of assets (cash) tantamount to release of accumulated profits