Get rich slowly

We have a really exciting announcement—scroll down to find out 😀

We’re almost at the end of the year, which means, it’s time for fresh starts. In this issue:

We talk about how to start your personal finance journey without losing your mind. As they say, starting is half the battle.

Compounding in everything.

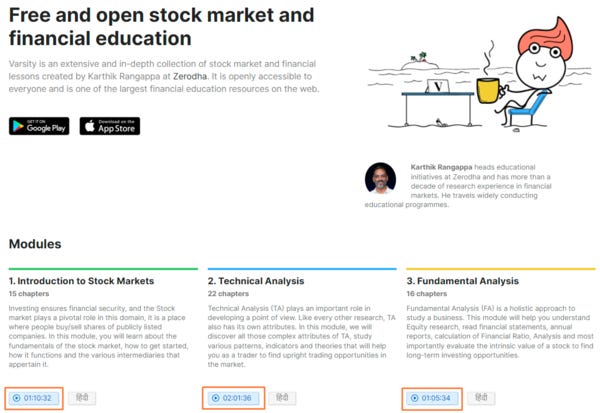

Introducing the Varsity video series

Educating people about investing is near and dear to our hearts at Zerodha. Karthik started working on Varsity 8 years ago, and today, it has over 180 chapters in English and Hindi. Karthik has also answered almost a lakh questions from investors and traders.

Over the year, one major request from all of you has been for a video version of Varsity. For the past several months, Karthik has been slogging away to create this, and we’re finally super excited to introduce the Varsity video series 😍

Videos for the first three modules are live, and we’ll keep adding more. You can find links to the videos on the homepage under each module.

Here’s a post from Karthik & Nithin talking about the backstory of Varsity and how the video series is structured:

Introducing Varsity Video Series – Z-Connect by Zerodha Z-Connect by Zerodha

Varsity has been a labor of love for us. We hope you enjoy and learn from the videos; we thoroughly enjoyed making them for you. If you have friends who keep saying that they want to learn about the stock market & investing, then you should send this to them. They won’t have an excuse anymore 😉

Slowly and then suddenly

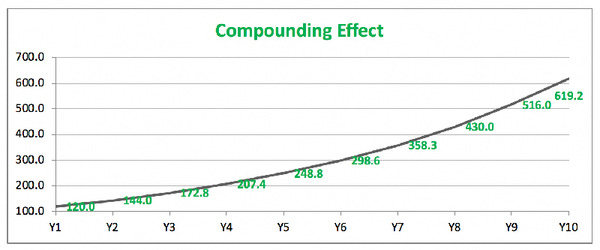

Last week was National Mathematics Day, and we wrote a Twitter thread about compounding—one of the most important formulas.

I’m sure you would have heard about compounding a thousand times. Phrases like the “magic of compounding” have almost become a cliché. But just because it’s a cliché doesn’t make it any true.

Small returns over a long period add up tremendously—enough for you to be shocked. Letting your money compound over decades without disturbing it is an underrated edge.

“A modest rate-of-return can accumulate a fortune over time. You don’t need to beat the market, do over-leveraging, or pick the best stock to be rich. You just need to earn a decent rate-of-return and let your money compound overtime.”

― Naved Abdali

People often speak about compounding in the context of investing, but it applies to pretty much everything in life, not just investing. Just like small returns can compound over a long period, small actions performed consistently can lead to amazing results.

Here’s how compounding looks like. Slowly and then suddenly 🚀

Take the example of fitness. Most people want to be fit, but obesity and heart disease are rampant. The key to being fit is pretty simple—eat well, exercise, sleep well and keep stress in check, but very few people do it consistently.

It’s partly because we want instant gratification—we hate thinking about the future. The other issue is that we think linearly and can’t wrap our heads around exponential growth.

Physicist Albert Bartlett put it: “The greatest shortcoming of the human race is our inability to understand the exponential function.”

― Morgan Housel

So, how do you compound in life?

First and foremost, you need to understand compounding. You also need to be able to think about tomorrow instead of today and have unyielding patience.

Building wealth slowly

We’re at the end of the year, and that means it’s time to make new year resolutions which we’ll never follow. One of the most popular new year’s resolutions is “I will start investing this year.” But countless new years later, only 2.5 crore Indians invest in mutual funds out of 138 crores. Clearly, people aren’t following their resolutions to start investing.

I’m sure all of you, like me, have countless stories of trying to do something and giving up midway.

Why?

I think we can draw lessons from the decades of research into how we form habits.

Intent and interest play a big role. You can’t do what you don’t like, no matter how hard you try. But one of the biggest reasons we give up when trying to learn something new is because of our misguided notion that we need willpower and self-control to learn something. That’s not the case. Research shows that habits and behaviours are the result of specific cues in certain contexts, not constantly pushing yourself consciously.

We form habits when we keep repeating the same action over and over again in a stable environment based on a cue. After a while, a routine becomes a habit, and you do it without even thinking consciously. Take the example of learning how to ride a bike. Once you learn, you start riding effortlessly without consciously thinking about it—it becomes muscle memory.

The key to forming a habit:

You need to be motivated. You can’t build a habit of doing something you hate.

Break it down into small actions.

Have a cue that triggers that action in a stable environment. For example, a sticky note or an alarm can be a cue to do something.

Repetition. You have to keep performing the action repeatedly. This routine will become a habit eventually.

Rewards. Find a way to celebrate small wins and reward yourself.

Let’s take the example of building a reading habit. Just forcing yourself to sit and read an entire book in a day is a terrible idea.

Instead, reading 10-20 pages a day and rewarding yourself when you finish reading every day is a much better approach. The reward could be something as simple as 10 mins of YouTube.

As you keep reading 10-20 pages a day, this routine slowly becomes a habit over months. After some time, you won’t even need a reminder. Your mind will automatically remember the specific time to read.

The reason why I’m writing about habits is that learning how to manage your personal finances is like building a habit. Good money habits can improve your life immensely, but bad money habits can be destructive.

Decades of research has shown that financial literacy leads to overall financial wellness. Financially literate people tend to build more wealth. They are better prepared for retirement, to deal with emergencies and income shocks. They’re also less likely to have costly debt and invest in toxic financial products. Financial literacy is also linked to overall physical and mental wellbeing.

It intuitively makes sense. For better or worse, money is central to our lives. Knowing how to manage money can help you make the right decisions not just with your money but also with that of your family and friends. The best part is that you’ll keep realizing the benefits of sound money decisions throughout your life―a bit like compounding.

When you have a good relationship with money, you are less financially stressed and anxious. Financial stress and anxiety are poorly understood, but serious issues today.

Coming back to the original point, how do you learn about money and personal finance?

Start small. Learn the basics of compounding, debt, investments and taxes slowly.

Starting your personal finance journey can seem scary, but that’s just at the start. I certainly was intimidated when I started, but that feeling quickly faded as I got my basics right―nothing fancy, just the basics.

80% of personal finance is getting the basics right. Have a specific financial plan, save enough for retirement, have insurance for protection, keep your costs low and don’t do anything stupid.

But you can’t do all those things in one go—it’s impractical. Going back to our earlier point, to build a habit, you need to break it down into small actions—it’s the same with your personal finances.

So, this new year, start small and start with the easy things. You can progressively build on it later.

The very first thing I would recommend you start with is by learning about what compounding is. Karthik has beautifully explained this in the first couple of chapters of the personal finance module.

Next, I would recommend that you check out this post where we had written about a really simple personal finance checklist.

Coin newsletter #3: Starting troubles – Z-Connect by Zerodha Z-Connect by Zerodha

The most common personal finance recommendation is to have an emergency fund. People usually recommend keeping 6-12 months of your salary in a liquid fund. This is to help you deal with unforeseen events like job losses. Otherwise, you’ll end up taking costly loans or run up credit card debt.

6-12 months is just a guideline. It really depends on the person and his or her unique circumstances. So don’t sweat the actual number, it’s whatever period that gives you peace of mind.

You can create an emergency fund by saving money in a liquid mutual fund or an ultra-short debt mutual fund. These are really simple funds, like bank fixed deposits (FD).

The goal of an emergency fund is not to generate returns but rather to help you deal with unforeseen shocks. Liquidity is important because you should be able to quickly withdraw this money in a pinch. Liquid and ultra-short funds are pretty liquid and perfect for this.

The other advantage of investing in a liquid fund is you’ll now be familiar with mutual funds. It might naturally push you to learn more about investing.

That’s it. You have completed two things on your personal finance checklist. You can celebrate this little win 😀

Things really are simple when you break them down into small action items. Over a period of time, you can slowly check off other things like getting term and health insurance for protection and investing for your retirement.

“If you are investing in your education and you are learning, you should do that as early as you possibly can, because then it will have time to compound over the longest period.

And that the things you do learn and invest in should be knowledge that is cumulative, so that the knowledge builds on itself.

― Warren Buffett

With that, it’s a wrap on this year. We’ll see you in 2022.

From all of us here at Zerodha, we wish you a very happy and prosperous new year 🥳