Fear of a sudden turn of events

Fear of a sudden turn of events

Issue #8

Hello folks, sorry for the radio silence, but the Varsity newsletter is back.

In this issue:

How to deal with the fear of trading

New video series on trading and investing concepts

Videos on the basics of options trading

Why are debt fund NAVs falling?

Personal finance: Where to save money for short-term goals.

Confronting your fears

It’s been a case of when it rains, it pours for the markets—pandemic, war, shortages of everything, rapid inflation, rising interest rates. There’s been a synchronized rise in inflation across developed and developing economies. In response, central banks around the world have started hiking rates aggressively. This has led to a repricing of equities around the world. Valuation multiples for the major markets have shrunk dramatically in just a few months.

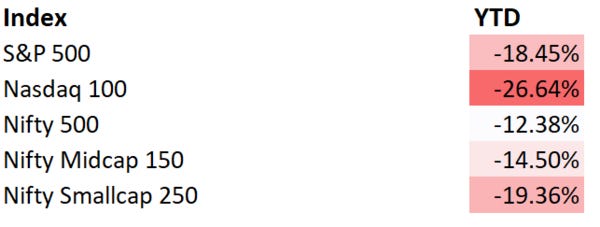

Though Indian markets haven’t fallen as much as the US, they’re down for the year.

It’s stunning how quickly the sentiment changed from unbridled optimism in 2021 to extreme pessimism in 2022. The markets have been quite volatile given the sharp fall in the markets and all the macro shocks. Such volatile phases aren’t easy to trade. Trading is a constant battle against greed and fear, and keeping a level head is extremely hard. But during market phases like these, traders are at a higher risk of being driven by their emotions than logic.

Most traders tend to have a heightened fear of losing money in markets like these. It’s important to understand why we’re afraid. Fear isn’t a bug, it’s a feature and a survival mechanism. Our ancestors were naturally programmed to run as soon as they heard a sound in the bushes. That’s how they survived and adapted. But when it comes to trading, fear can not just paralyse and stop you from taking trades, but it can cause you to make costly mistakes. This reminds me of a humorous quote:

“How did you go bankrupt?“ Two ways. Gradually, then suddenly.” — Ernest Hemingway

But if you want to be an active trader, you must learn how to deal with your fears and have a plan. It won’t be easy, which is why only 1% of traders make any money. But how do you deal with fear when trading?

There’s a brilliant Innerworth post on this:

The first step in conquering fear is to merely admit that you are afraid. A second way to manage fear is to trade small positions. The less money on the line, the less risk you are taking, and the less fear you are likely to experience. Third, manage risk. By using protective stops and by risking only a small percentage of capital on a single trade, you will feel more at ease and can more easily manage fear. Fourth, you can trade more cautiously by making sure that your trading plan is consistent with a broader trend.

Fear of a Sudden Turn of Events – Varsity by Zerodha

Varsity Bytes

We started a new video series called Varsity Bytes. In every video, Karthik will explain trading and investing concepts that most people get confused with. In the first video, he explains how to decide between buying a call and selling a put when you’re bullish on a stock.

Varsity video series

We’ve published 11 videos on options trading. The latest video is on physical settlement, check them out 👇

Why are my debt fund NAVs falling?

When building portfolios, most investors focus too much on equity funds and very little on debt funds. In fact, a good segment of investors doesn’t pay attention to their debt portfolio at all. They choose funds based on star ratings, best fund lists or random recommendations. Very few investors actually spend time understanding the basic concepts.

Investors also don’t understand concepts like yield, duration and the impact of interest rates on debt funds. The problem with investing in something you don’t understand is that you won’t have the conviction to hold it when times are bad. This is the biggest reason why investors buy and sell at the wrong time. It’s the same issue with debt funds.

Given the inflation and rising interest rates, debt fund NAVs have taken a hit. Over the last couple of months, “why are my debt fund NAVs falling?” has been the most frequent query from mutual fund investors.

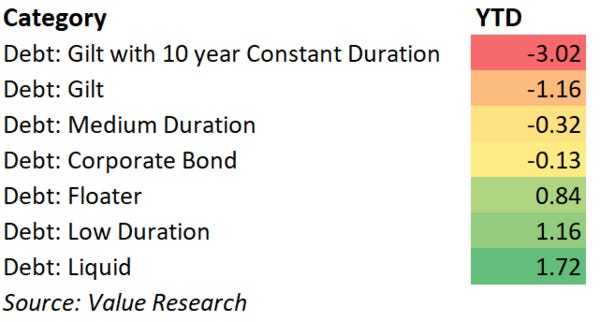

Here’s a quick snapshot of short, medium and long-duration funds.

Debt funds and interest rates have an inverse relationship. When interest rates fall, debt funds do well and when interest rates rise, they perform poorly. But the impact isn’t uniform—it depends on the duration of a fund. The shorter the duration, the lower the sensitivity to interest rate changes.

We recently published two threads explaining some of the basic concepts of debt funds that every investor should know.

We also recorded a podcast with Mahendra Jajoo, the CIO of fixed income at Mirae Asset India, on the same topic. Listen to it here 👇

Why are debt fund NAVs falling? - Zerodha Educate | Podcast on Spotify

Personal finance tip

Thanks to social media, everybody is an expert on personal finance. The amount of horrible and downright dangerous advice on personal finance is scary. I recently saw a post about where to save money for short-term goals. The advice in the post was that investors willing to take high risk can invest in instruments with higher credit risk to generate higher returns for short-term goals. Credit Risk is a fancy term for the possibility of losing money.

This is extraordinarily stupid advice. When it comes to short-term goals under 5 years, the safety of the capital is more important than returns. It might sound obvious, but plenty of people go wrong with this. Let’s look at a simple example.

Let’s say, you want to go on a vacation after 3 years and the cost is 1 lakh. Since this is a really short-term goal, keeping this money in equities makes no sense. Why? What if the market falls 30% just before your travel date? So, the best place to keep this money is in overnight or liquid funds. These funds have returns similar to savings bank and FD rates, but safety is more important than returns.

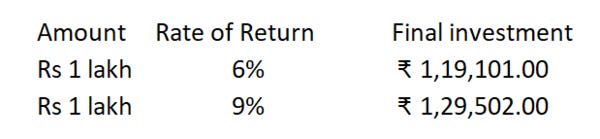

Let’s say the return on a liquid fund is 6% and there’s a short term debt instrument with 9%. What should you choose? Let’s look at the returns.

Before you say, you should obviously choose the 9% instrument, remember, in debt instruments, higher returns always mean higher risk. Higher risk is nothing but a higher chance of losing your investment. More importantly, the chances of recovering losses in debt funds are almost zero.

Does it make sense to take a higher risk just to make an extra return of Rs 10,500? Absolutely not! For short-term goals and your emergency funds, the return of capital is more important than the return on capital. Don’t chase returns with this money, it’s not worth it.